Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

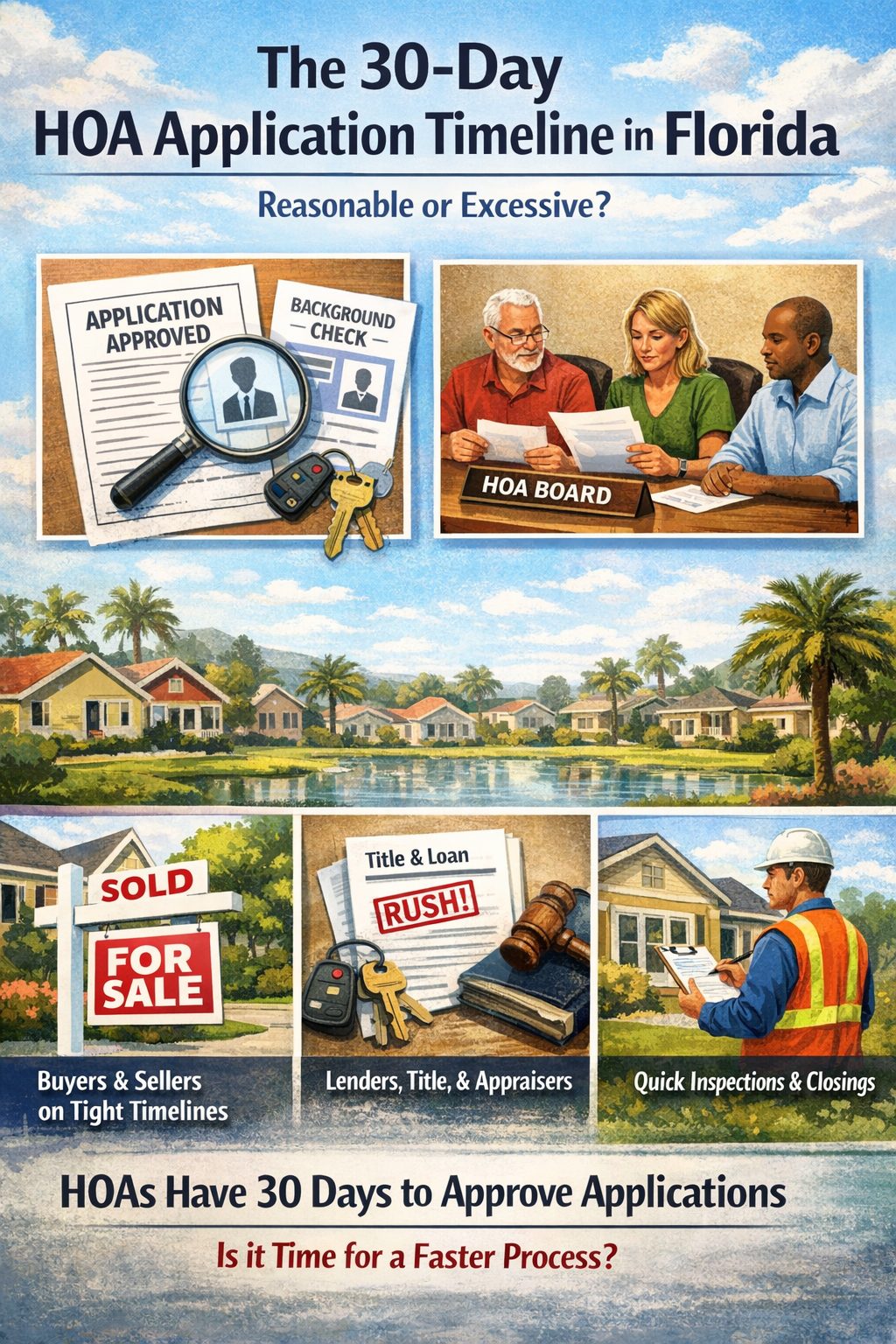

If you have ever bought or sold a home in Florida that is governed by a homeowners association, you know the waiting game that can follow once a contract is signed. In our state, HOAs typically have up to 30 days to process and approve (or deny) an application.

Let me start by saying this: I empathize with HOA board members.

I served on an HOA board for years. It is a volunteer position. It is often thankless. And at times, it feels like a second full-time job. You deal with budgets, maintenance issues, violations, vendor contracts, and neighbor disputes. I understand firsthand that it is not easy, and most board members are simply trying to protect their community and property values.

That being said, we need to have an honest conversation about the 30-day timeline.

In a typical real estate transaction, the buyer is on strict deadlines from day one. Inspections are usually completed within 7 to 10 days. Loan approval often must be secured within 21 to 30 days. Lenders, title companies, appraisers, and even government departments responsible for lien searches and title searches all operate on tight timelines. If they do not, deals fall apart.

These parties are handling complex financial underwriting, property valuation, compliance, title review, and legal documentation. They are responsible for significantly more moving parts and liability than simply reviewing an HOA application.

Yet the HOA often has the longest window of all.

Here is what the process typically looks like:

- The buyer submits the completed application to the management company.

- The management company runs the background checks.

- The full application and background report are presented to the HOA board.

- The board reviews criminal history (if any), verifies vehicle information, confirms pet compliance, and ensures the applicant meets community guidelines.

- A decision is made.

That is it.

In most communities, this is not a complicated underwriting process. It is a review process. The heavy lifting (background screening) is usually outsourced and completed quickly.

So why does it take up to 30 days?

When a transaction is held up by HOA approval, everyone feels it:

- Buyers who have locked in interest rates and scheduled movers

- Sellers who are coordinating their next purchase

- Lenders managing rate expirations

- Title companies and attorneys preparing closing packages

- Appraisers and inspectors working within contract deadlines

A delayed approval can push back closing, create stress, and in some cases, jeopardize the entire transaction.

Again, I understand the volunteer nature of HOA boards. I respect it. I have lived it. But if lenders can underwrite a six-figure or seven-figure loan in three weeks, and title companies can clear ownership and lien issues in less time, it raises a fair question about whether 30 days should be the norm for an application review.

Most of the time, these applications do not require deep investigation. They require organization, timely communication, and a scheduled review.

I believe HOAs can protect their communities while also respecting the realities of modern real estate timelines. Shorter review windows, more frequent board review cycles, or delegated preliminary approvals (where appropriate) could go a long way toward making the process smoother for everyone involved.

The Florida market moves quickly. Buyers and sellers are operating under intense financial and contractual pressure. A more efficient HOA approval process would not just help real estate agents. It would help homeowners.

And at the end of the day, that is who HOAs exist to serve.